EPJ B Highlight - Understanding stock market returns: which models fits best?

- Details

- Published on 27 March 2019

A comparison of two models for stock market prediction shows clear differences in their accuracy, depending on the length of the forecasting period

Understanding stock market returns hinges on understanding their volatility. Two simple but competing models have been dominant for decades: the Heston model, introduced in 1993, and the multiplicative model, which dates back to 1990. American physicists recently compared the two models by applying them to the United States stock market and using historical data from two indexes: the S&P500 and Dow Jones Industrial Average. In a study published in EPJ B, Rostislav Serota and colleagues from the University of Cincinnati, OH, USA, demonstrate the clear differences between the two models. Simply put, the Heston model is better for predicting long-time accumulations of stock returns, while the multiplicative model is better suited to predicting daily or several-day returns.

Stock volatility depends on the level of randomness associated with the statistical dispersion around a central stock value--known as stochastic volatility. The Heston model predicts short tails for distributions of volatility and stock returns, which correspond to a low number of occurrences of values around the central return value. In contrast, the multiplicative model yields “fat” tails, governed by power laws, with a broad distribution around the central value.

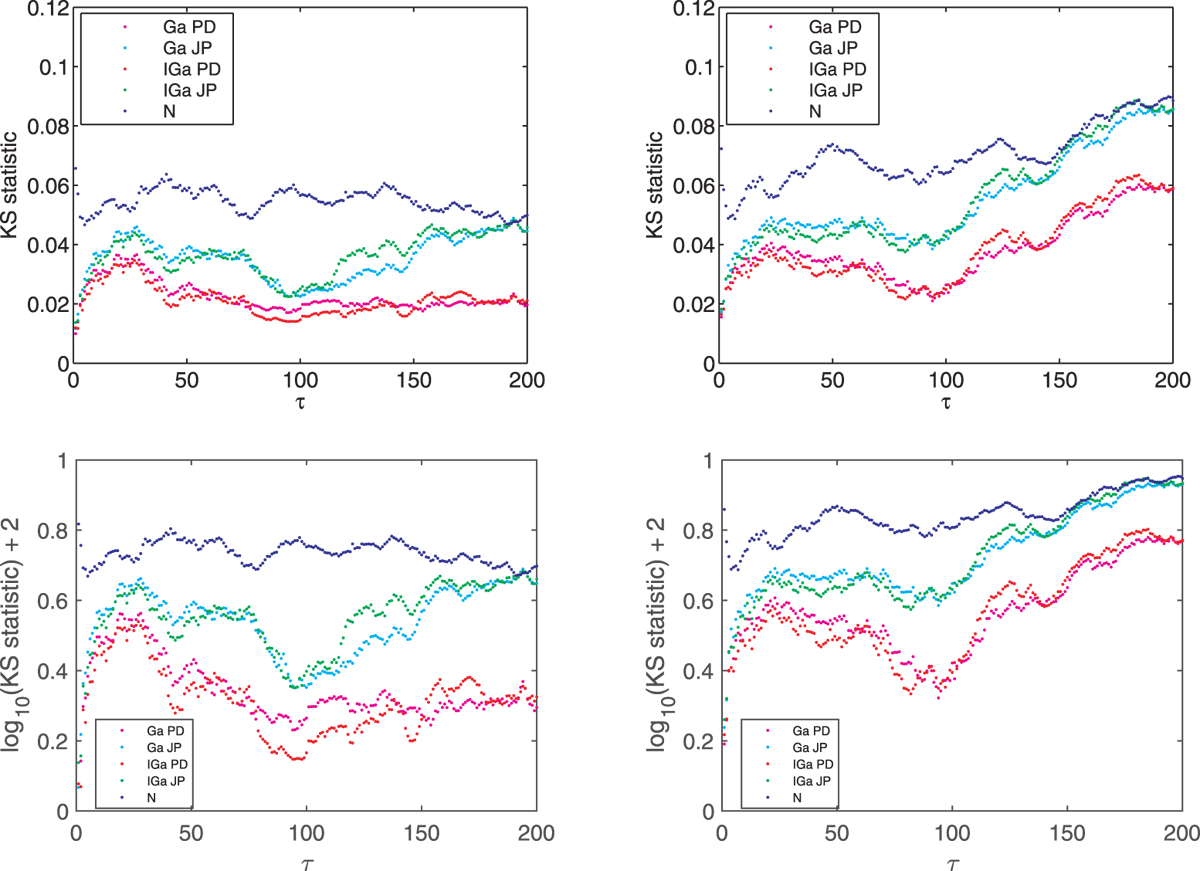

The team studied the moments of the distribution as a function of the number of days over which the returns were accumulated. According to the authors, this approach produces more definitive results that fitting the distributions of returns.

In follow-up research, Serota and colleagues are now looking for alternative models that combine the respective strengths of the Heston and multiplicative models. They have already completed a simple Heston-multiplicative model and are now working on its generalisation. In addition, they are exploring other characterisation properties for stock return prediction, such as leverage, correlations and relaxation.

Zhiyuan Liu, M. Dashti Moghaddam and R. A. Serota (2019), Distributions of Historic Market Data – Stock Returns, European Physical Journal B 92:60, DOI: 10.1140/epjb/e2019-90218-8